- Consolidated Revenue up 47% and Net Profit is up 782% YoY

- EBIT Margins at 14% Vs 5% YoY

- Cash Balance Rs.434 Cr as on 30th Sep 2022

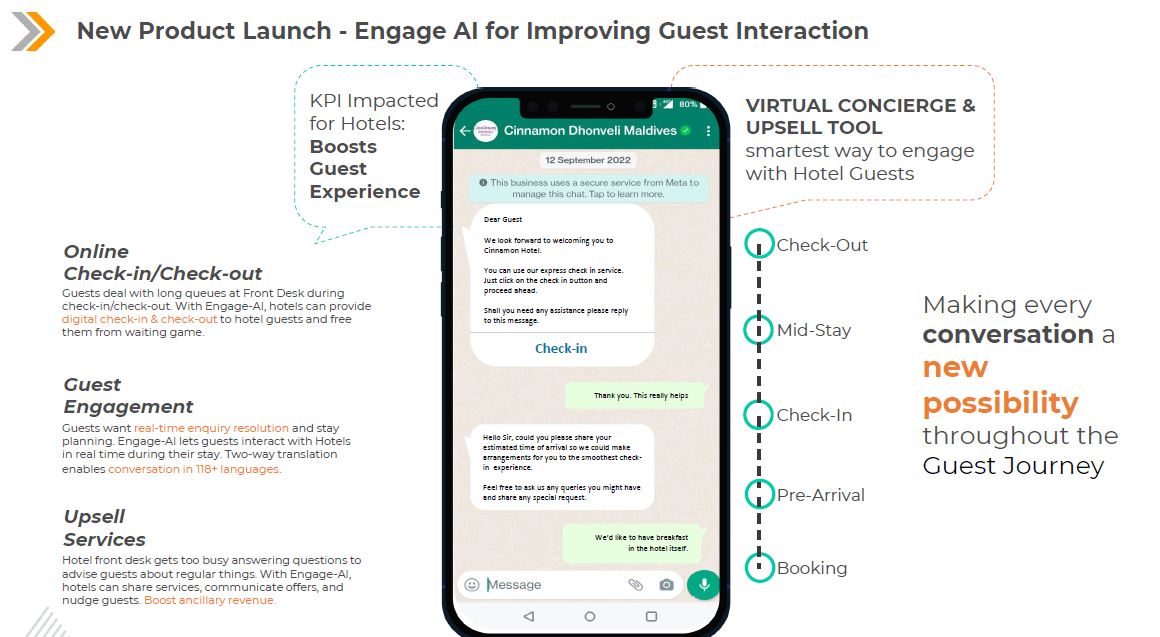

- New Product Launch – Engage AI

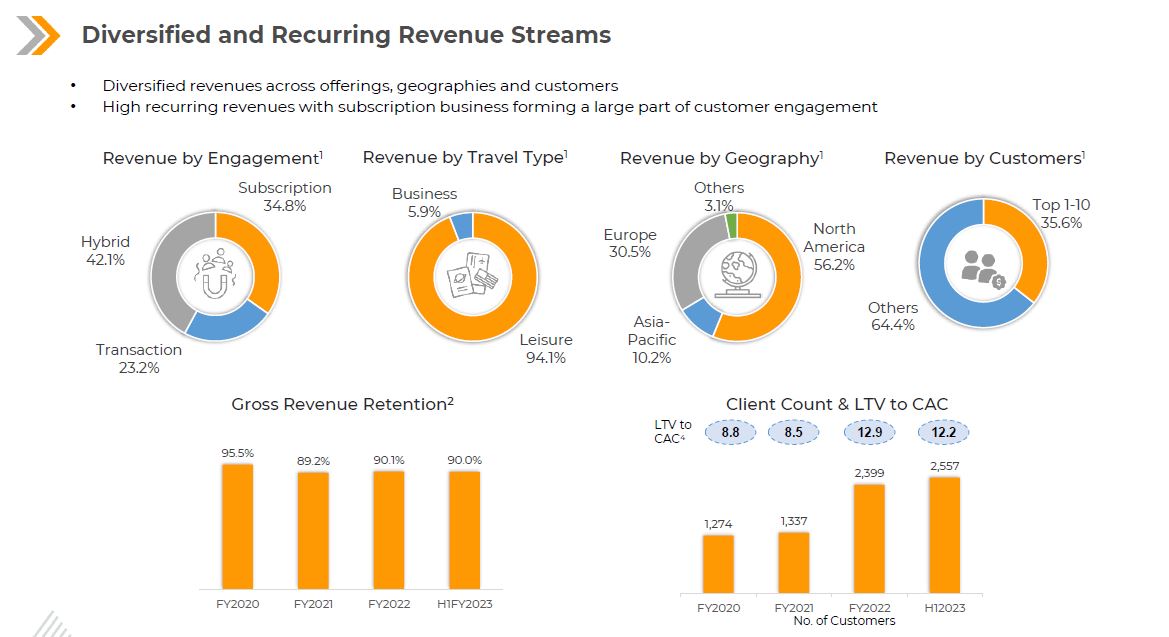

- Revenue Model – Subscription 34.8%, Hybrid 42.1%, Transaction 23.2%

- Revenue by Geography US 56.2%, Europe 30.5%, Asia 10.2%, Other 3.1%

- Top 10 Customers constitute 35.6% of Revenue

- Gross Revenue Retention 90% (% of renewed revenue vs last fiscal)

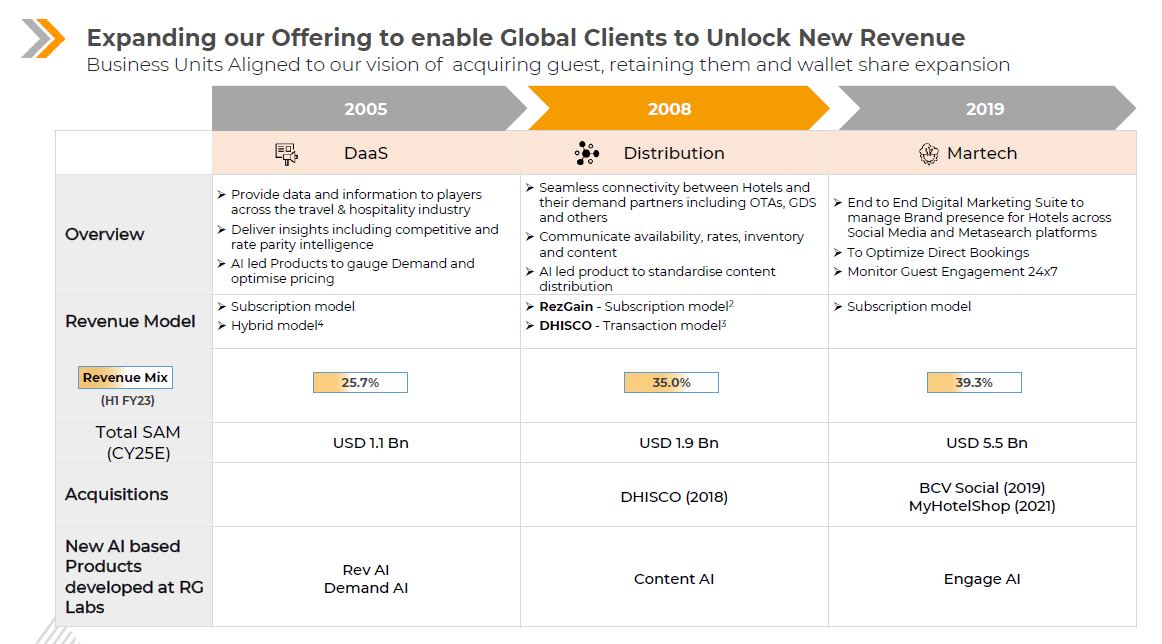

- Rategain Offerings and journey – DaaS, Distribution and Martech

- In H1FY23 DaaS contributed 25.7%, Distribution 35% and Martech 39.3% to total revenue

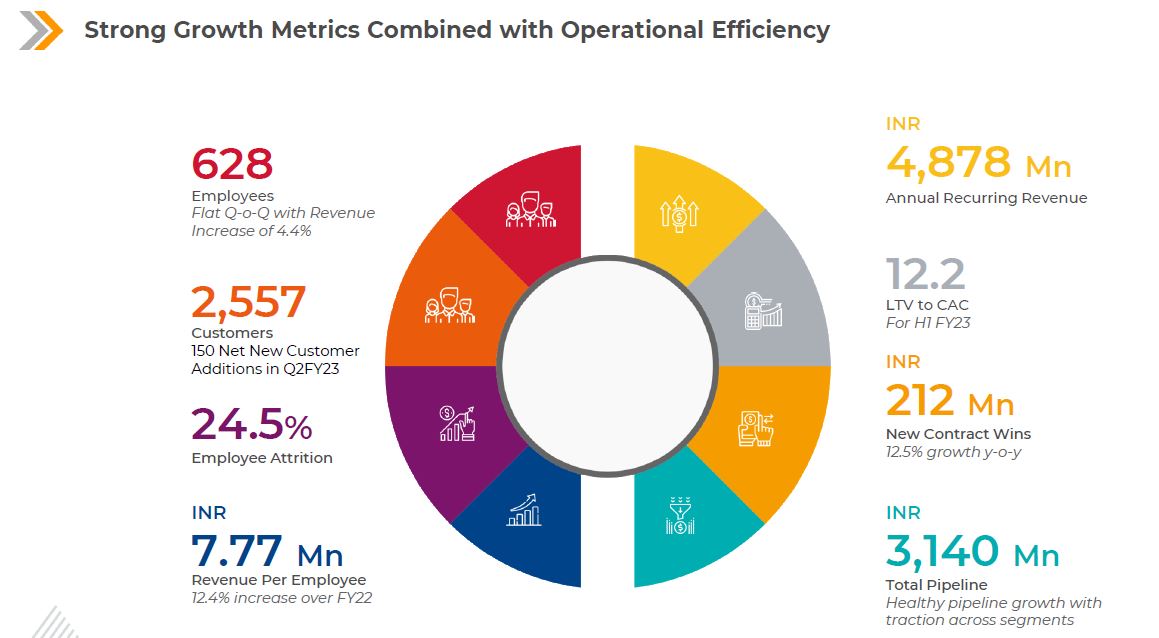

- Added 150 Net New Customer in Q2FY23, Total number reach to 2557

- Employee cost remained flat QoQ, DaaS and Distribution business shown better growth helped in kicking in operating leverage. Margins target is to reach EBITDA margin of 20-25% by FY25

- H2 will be stronger than H1 so similar margin of 15% can be expected.

- Analysing some M&A opportunities present in Market.

- Leading Airlines Air India and Akasa Air selected Rategain, So now almost all Indian Airlines are Rategain client. In last quarter Royal Orchid has also tied up with Rategain

Source: