- In Q4 Consolidated Revenue 8.9% and Net Profit up 31.85% YoY

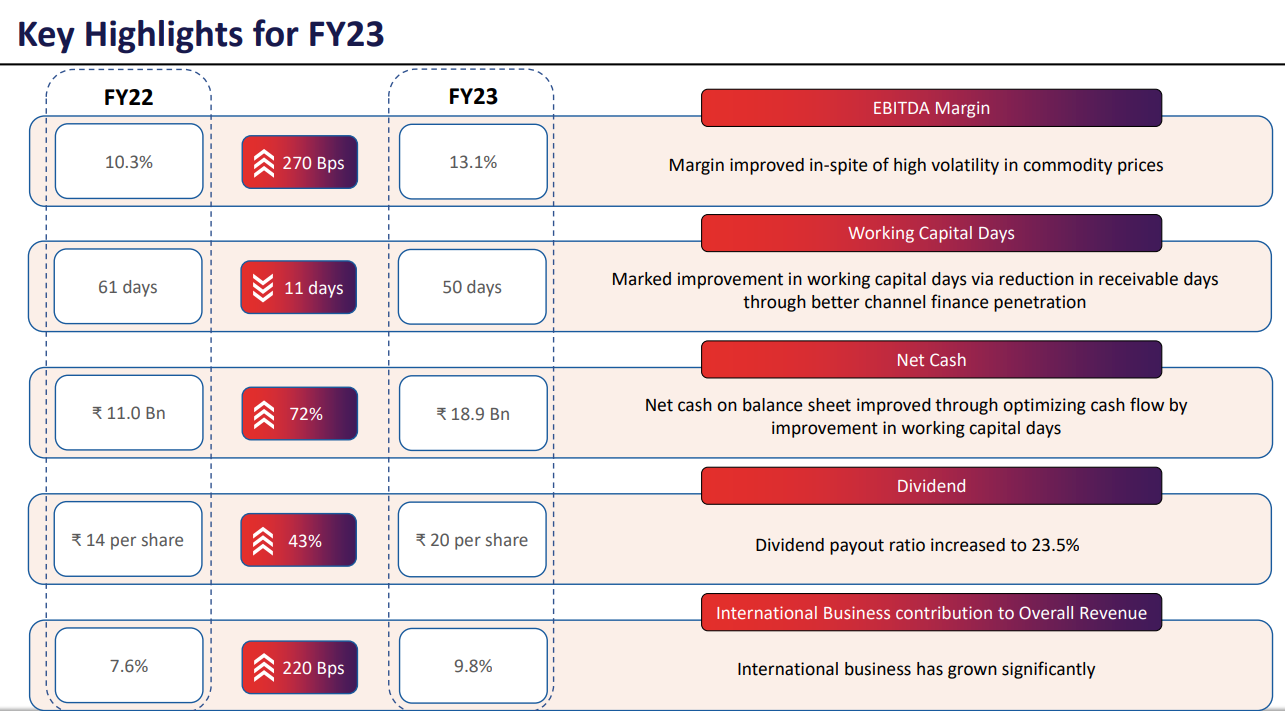

- EBITDA Margins at 14% from 12% YoY

- EBITDA margins improvement is due to favourable business mix, price hikes, better operating leverage and strong growth in International Business (International Business having margins 400bps above normal margins depending upon product mix)

- Net Cash Position Rs.18.9 Bn from Rs.11 Bn YoY

- Product Mix: Wire and Cables 89%, FMEG 9% and Others 2%

- Cables margins are in range of 10% to 11% where as wire business having margins of 14% to 15%

- Current mix of Wires and cables in business is 70% Cables and 30% wires

- Business Mix target by FY26 is 50:50 B2B (Cables & EPC) 50% and B2C (Wires and FMEG) 50%

- Domestic Sales contributes 90%, International 10% (US contribution is above 50%)

- Currently at International levels, we are among the top 50 wire and cable business. Target is to be in Top 5

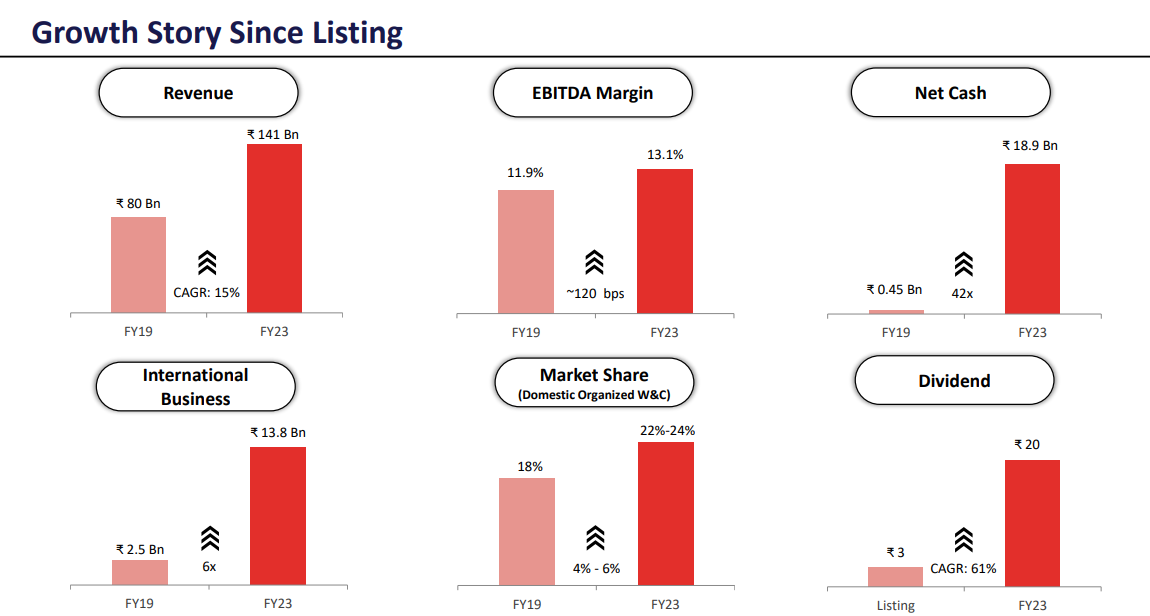

- Growth since Listing in 2019

- Soft growth in FMEG business in FY23 and degrowth of 20% YoY in Q4FY23

- EBIT in FMEG turned negative due to higher A&P, staff cost and input cost pressure. Company is confident for 10%-12% annualized EBITDA margin in this business by FY26

- Price hikes taken in mid-single digits range

- Capex for CY23 will be Rs.600 to Rs.700 Cr

- Capacity Utilization in FY23 for Wire and Cables is 70% and for FMEG it will vary product to product

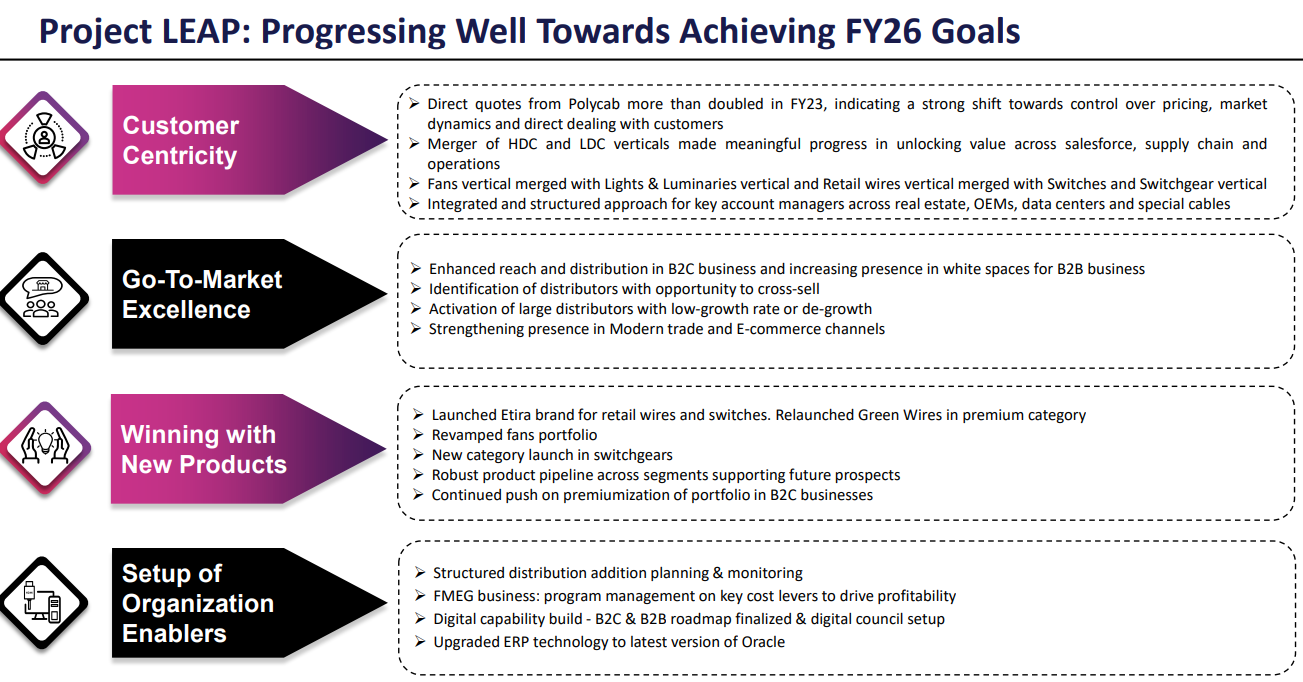

- Project Leap Progress

Source: