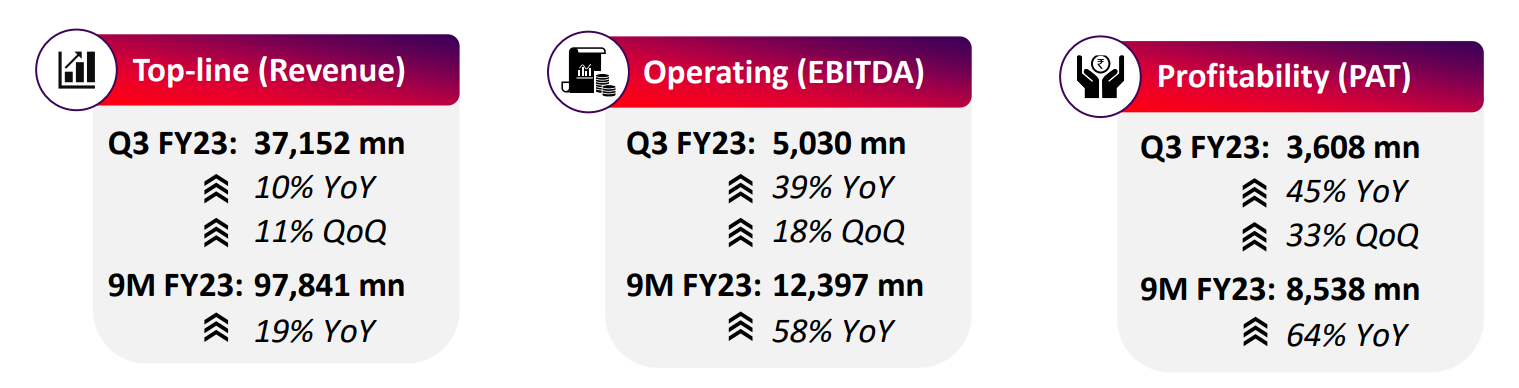

- In Q3 Consolidated Revenue 10% and Net Profit up 44% YoY

- EBITDA Margins at 13.5% from 10.7% YoY

- Net Cash Position Rs.18.7 Bn from Rs.6.7 Bn YoY

- Cash will be utilized in four ways either in capex, M&A activities, some retained as war-chest and rest will be distributed in shareholder as dividend and buybacks

- Revenue from Export shown growth of 32% YoY. Export Contribution to Revenue 5.9% from 8.1% YoY. With strong order book, expectation of 8-10% to FY23 consolidated revenue

- Company has achieved highest ever quarterly PAT in this quarter

- Interested in entering in High Voltage and Extra High Voltage and will put capex for EHV (Extra High Voltage) cables in Halol and expect production to get started in 2025 (In India KEI Industry is leading player in this segment)

- Being EHV is high technology product so we have tied up with Swiss company brugg cables for technology procurement

- Taking into consideration all these factors our capex from Jan 2023 to Dec 2023 will be Rs.600-700 Cr

- 3/4th of this capex will be utilized for wire and cable and 1/4th for FMEG

- Revenue from Wire and Cable shown growth of 11% YoY

- FMEG business remained flat YoY. FY23 should be considered as base year for FMEG business.

- Expecting better demand in Q4 FY23

Source: