- In Q2 Consolidated Revenue 10.8% and Net Profit up 37% YoY

- EBITDA Margins at 12.8% from 9.7% YoY

- Net Cash Position Rs.16.7 Bn from Rs.8.7 Bn YoY

- Wire & Cable revenue growth 13%

- Strong Export growth of 75% YoY led by USA, Europe and Asia. Strong demand from Oil & Gas, Renewables and Infra. Export is 13% of Consolidated Revenue of Q2 FY23.

- De-growth in FMEG Business 12% YoY

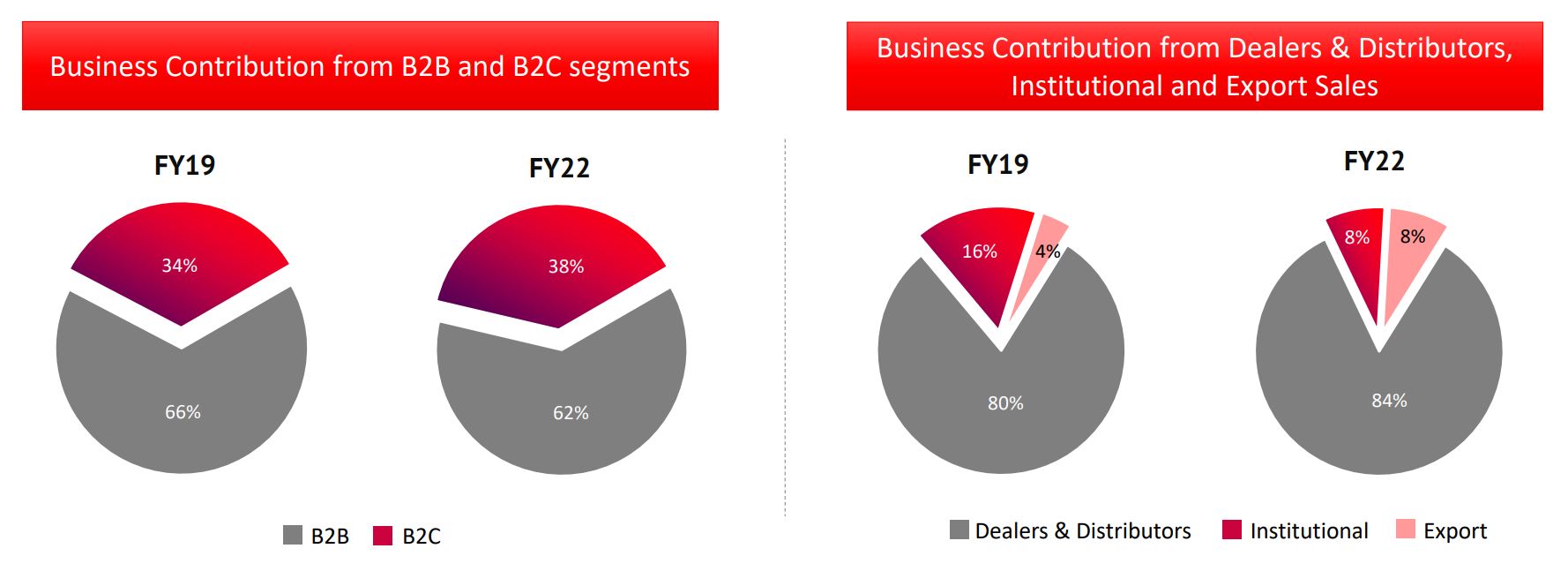

- B2B Vs B2C is 62:38 in FY22 from 66:34 in FY19

- Business contribution from Dealers & Distributors (84%), Institutions (8%) and Export (8%) in FY22

- Growth in Revenue is driven by volume growth mainly from wire and cable business

- Price Reduction due to decrease in commodity price is lower than benefitted from procurement of raw material

- 400 Cr Capex is expected in this year too. 2/3rd for Wire & Cable and 1/3rd for FMEG

- Will use cash in Capex, M&A & keep increasing dividend payouts

- Export business is sustainable and having similar margins

- Rural focused new Brand Etira contributing double digit growth in Retail wire business

- Capacity Utilization in Wire & Cable is 65% to 70%

- Project Leap Progress

Source: