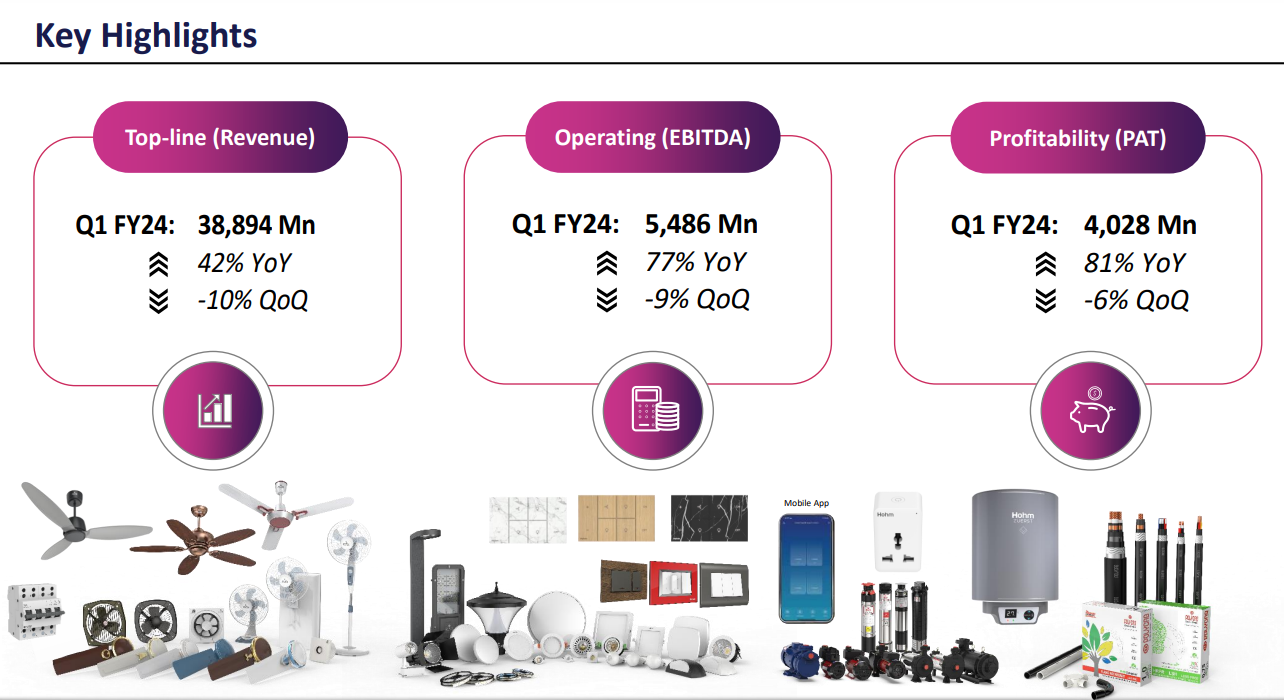

- In Q1 Consolidated Revenue 42% and Net Profit up 81% YoY

- EBITDA Margins at 14.1% from 11.3% YoY

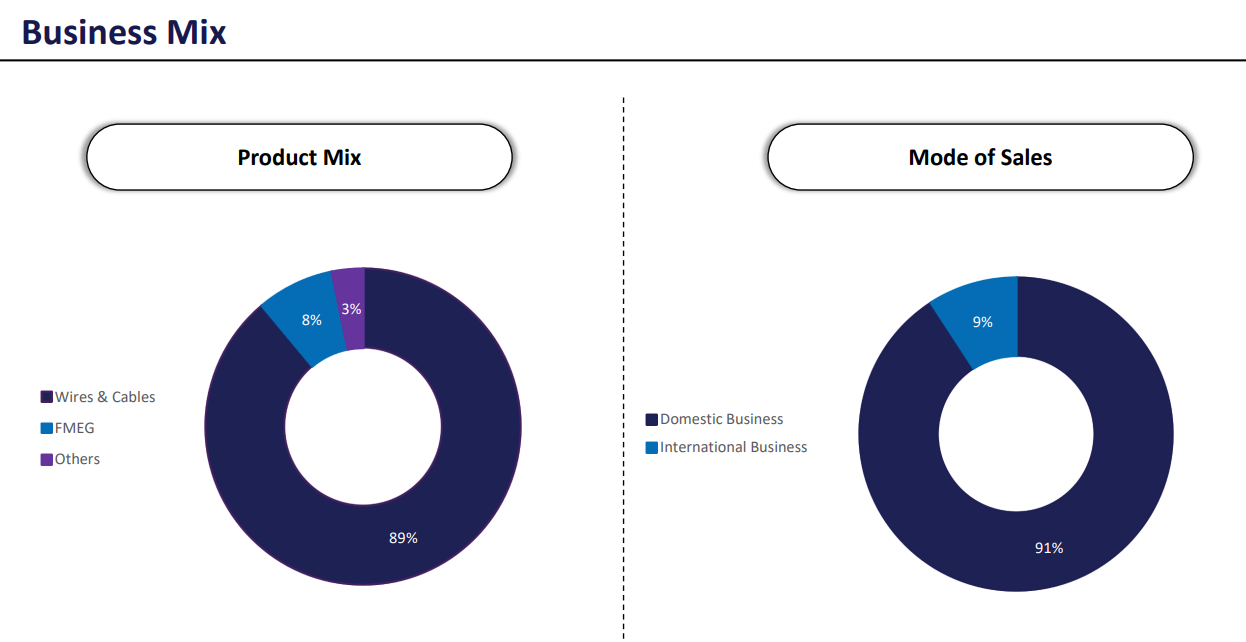

- Product Mix: Wire & Cable – 89%, FMEG- 8%, others – 3%

- Geographical: Domestic Business – 91%, International Business – 9% with combined volume growth of 50% to 60%

- Robust domestic demand supported by govt measures, improving private capex, strong real-estate off-take.

- Cable growth continue to outperform wire growth

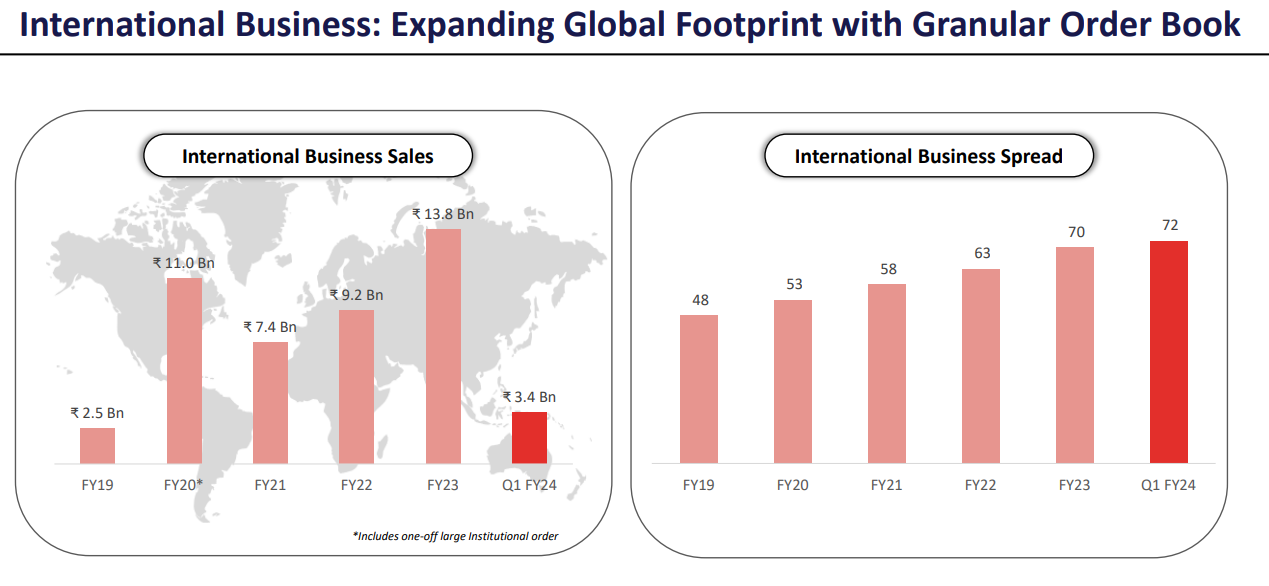

- International business revenue grew by 88% YoY. Company expanded its global footprint to 72 countries.

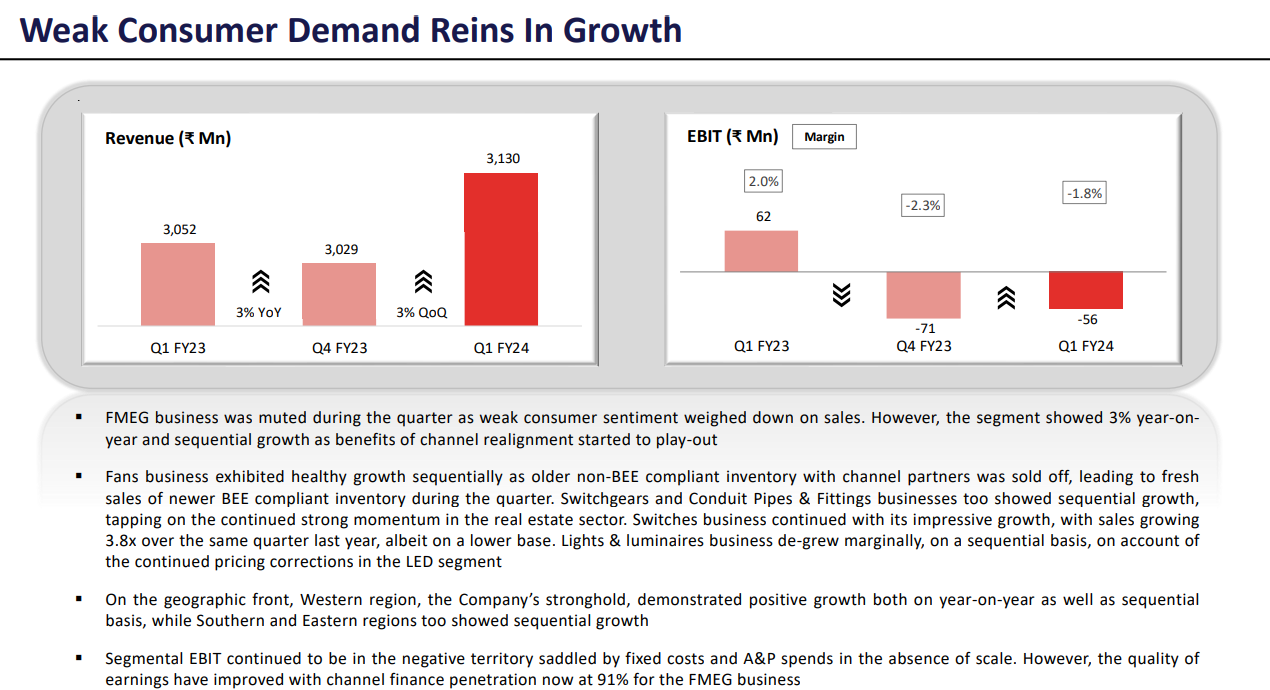

- Weak consumer demand in FMEG segment.

- Negative EBIT from FMEG segment due to lack of scale with fixed cost and A&P spends

- Expecting to achieve 10% EBITDA margins by FY26 from FMEG segment

- Net Cash Position Rs.10.13 Bn as against Rs.5.9 Bn YoY but was Rs.18.9 Bn last quarter. Cash will be utilized for Capex, dividend payment and any M&A opportunity.

- Capex guidance Rs.600 Cr yearly.

Source: