- Q2 Consolidated Revenue up 105% YoY and Net Loss Rs. 187 Cr

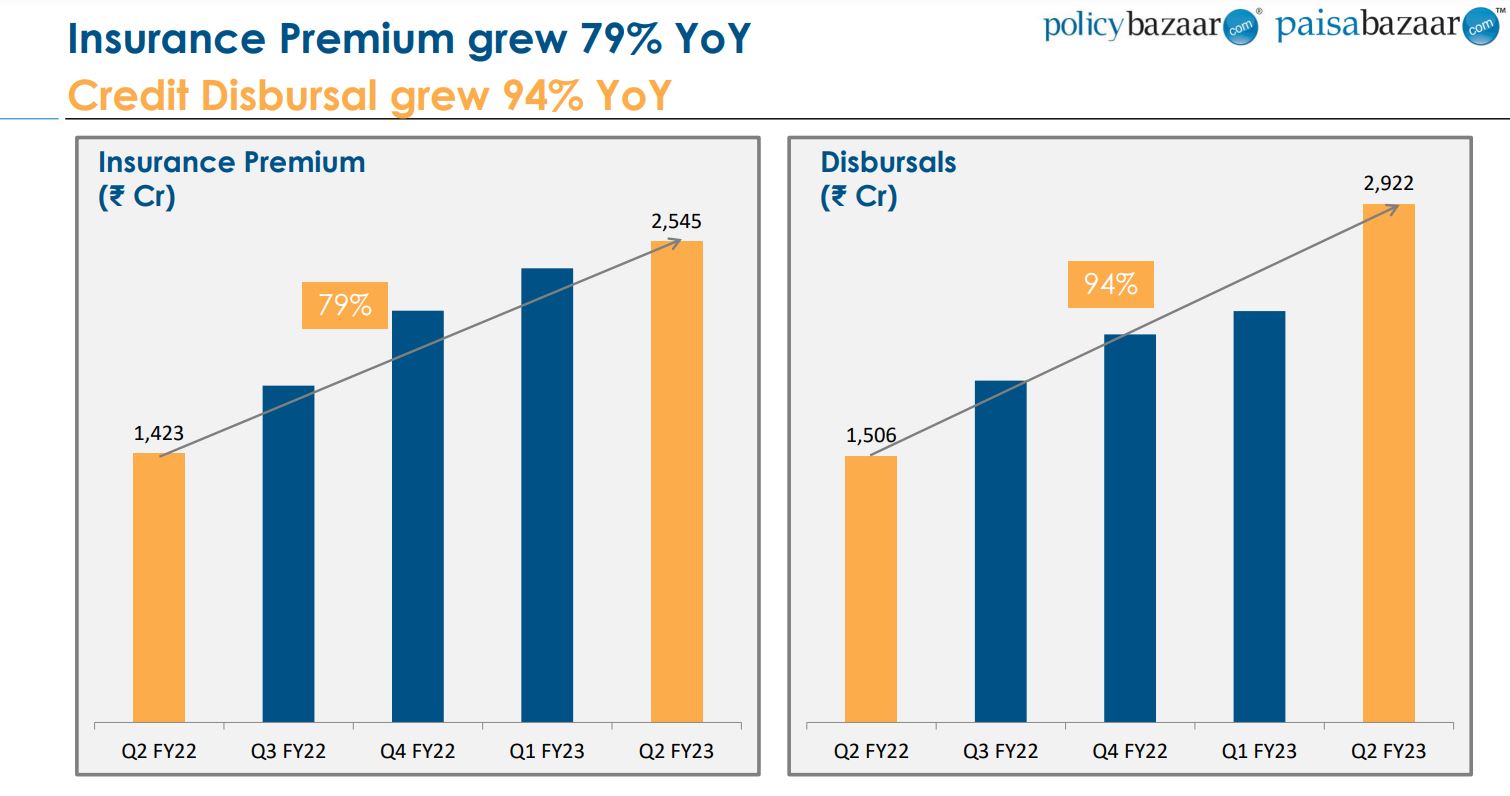

- Insurance Premium Rs.2545 Cr, up 79% YoY, Credit Disbursal Rs.2922 Cr, up 94% YoY. Contribution Margin 45% (Contribution = Revenue – Direct Cost (Employee Direct Cost + Acquisition Marketing)

- Core Business (PolicyBazaar & Paisa Bazaar) growth in revenue 55%, Core Insurance Business Adjusted EBITDA Positive with Rs.18 Cr. Non-Insurance (Paisa Bazaar still have loss of Rs.5 Cr)

- New Initiatives: PB Partners (POPS), Corporate & SME Insurance and UAE

- New Initiative Revenue at Rs. 164Cr, about 10 times YoY, Investment in new initiative is Rs.65 Cr (Rs.71 Cr in Q1 FY23 and was Rs.90 Cr in Q4 FY22) and may be just Rs.35 Cr from coming quarter. Going forward investment in new initiative will be below Rs.200 Cr

- New Initiative should break even by Q4 FY24

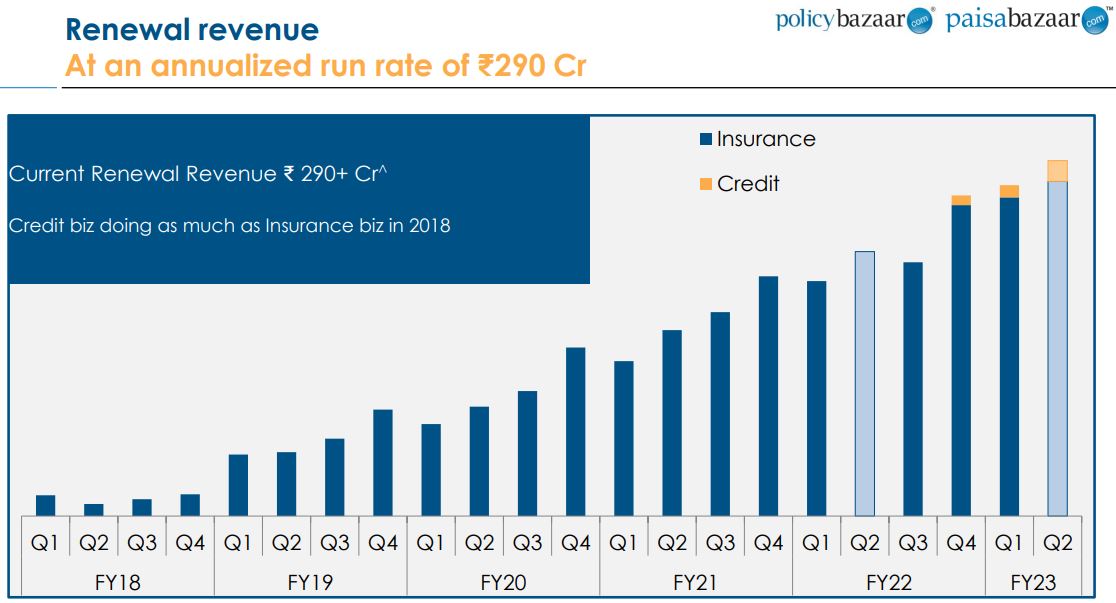

- Renewal Revenue at annualized rate in Q2 FY23 is Rs.290 Cr (was Rs.270 Cr in Q1 FY23 , Rs.260 Cr in Q4, Rs.210Cr in Q3 FY22) which has 85% Margins (in Q3 Co was claiming to have margins of above 90%, in Q4 last quarter claimed 87% to 90% and now saying having 85% margins). Now Credit Biz has also started giving renewal commission revenue which was unexpected to management

- Confident on Adjusted EBITDA positive by Q4 FY23

- ESOP Cost of 60% will be expensed by March 2023 and later 40% in next 3 years. In this quarter ESOP Cost is Rs.173 Cr

- Bima Sugam – Positive move for industry. We will get data layers which may or may not have today. Need more clarity going forward about how Bima Sugam will evolve.

- Cash Reserves as on 30th Sep 2022 is Rs. 5000 Cr. Cash plus receivables will not loose from these levels. Last quarter we have not burnt any cash.

- Company is aiming for Rs.1000 Cr PAT by FY26-27

Source: