- Consolidated Revenue up 30.6% and Net Profit 27.6% YoY

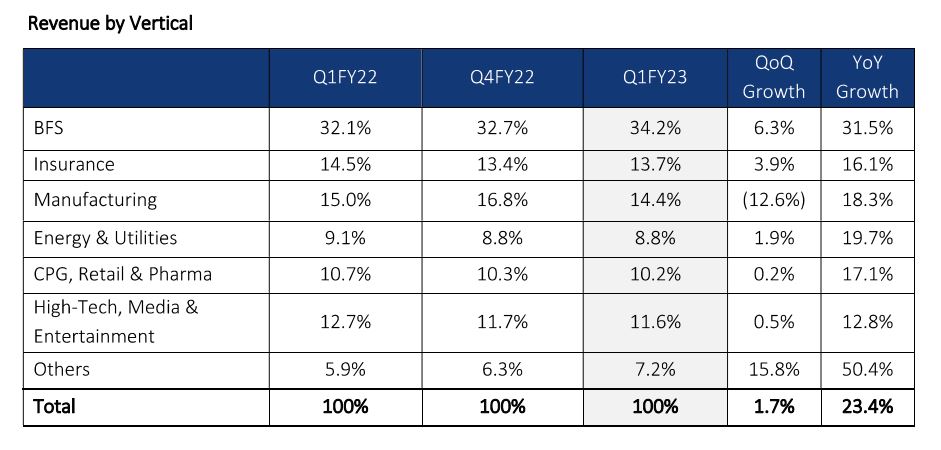

- Revenue by vertical in this quarter BFS- 34.2%, Insurance- 13.7%, Manufacturing- 14.4%, Energy & Utilities- 8.8%, CPG, Retail & Pharma- 10.2%, Media & Entertainment – 11.6%, Others- 7.2%

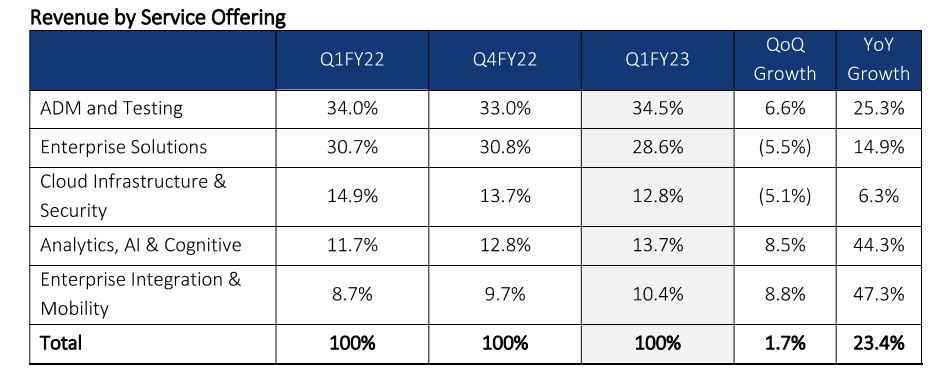

- Revenue by service offerings Application Data Management (ADM) and Testing- 34.5%, Enterprise Solution- 28.6%, Cloud Infra & Security- 12.8%, Analytics, AI & Cognitive- 13.7%, Enterprise Integration & Mobility- 10.4%

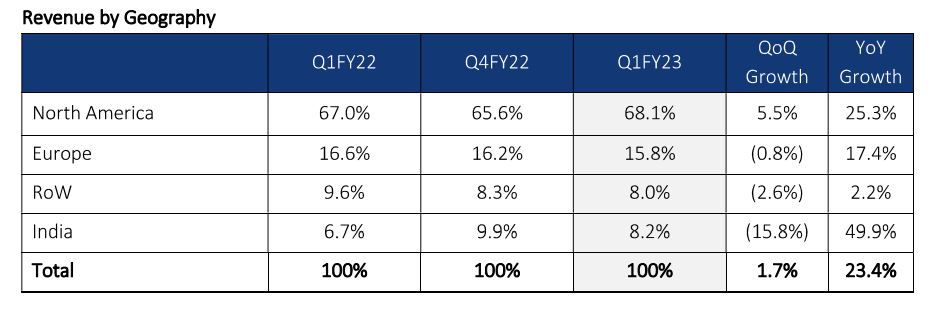

- Revenue by Geography US- 68%, Europe- 15.8%, India- 8.2% and Rest of the World- 8%

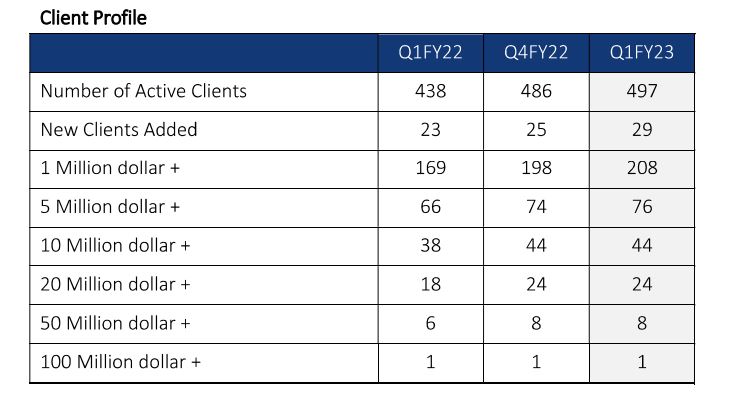

- Client Contribution to Revenue Top 5 Clients 29%, Top 10 Clients 40.4%, Top 20 Clients 55.7%. Number of active clients Q1FY23 is 497 (Added 29 Clients in this Quarter)

- EBITDA Margins 16% Vs 17.3% in Last Quarter

- Margin pressure due to higher employee cost post wage hikes, increase travel and visa cost. Some margin pressure offset by productivity benefit & INR depreciation.

- Attrition Rate 23.8% Vs 24% Last Quarter

- Closed 4 Large Deals with Net New Total Contract Value (TCV) of $79Mn

- LTI has been named GSI Global Delivery Platform Partner of the Year by Snowflake – Award demonstrate LTI execution expertise across strategy migration and modernization on Snowflake data on cloud.

- Building for a strong Q2 based on acceleration in demand across client base. Positive on closing large deals in Q2 as well.

- Expecting stable PAT margins in range of 14-15% for FY23

- BFS is in multi-year technology modernization cycle and we have strong hold in this category. Growth in this category is 31.5% YoY.

- Not seeing any project cancellation or project delay as of now, No sharp drop in demand as yet, but clients are looking for efficiencies now