- Q2 Consolidated Revenue up 28%, Net Loss Rs.2 Cr

- EBITDA Margins 4.89% Vs 5.84% YoY

- Net Loss is due to increase in Interest cost from Rs.6 Cr last year to Rs.24 Cr due to increase in debt for capex

- Total Debt at present is Rs.1311 Cr and Cash & Investment Position is Rs.645 Cr

- Out of total Revenue of Rs.750 Cr – Amber – Rs.328 Cr and Subsidiaries Rs.422 Cr

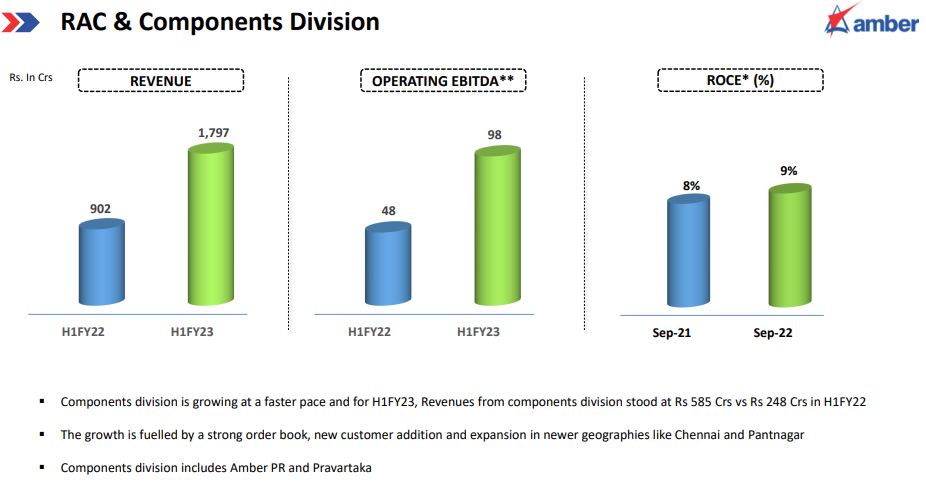

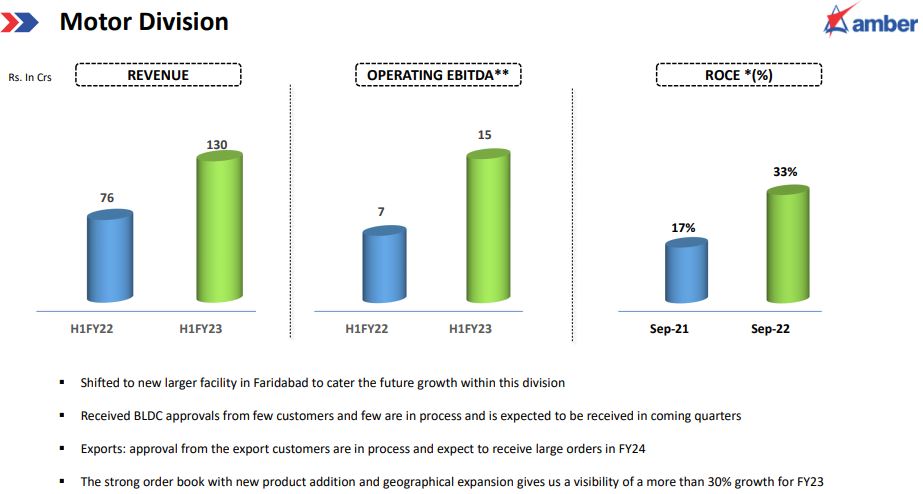

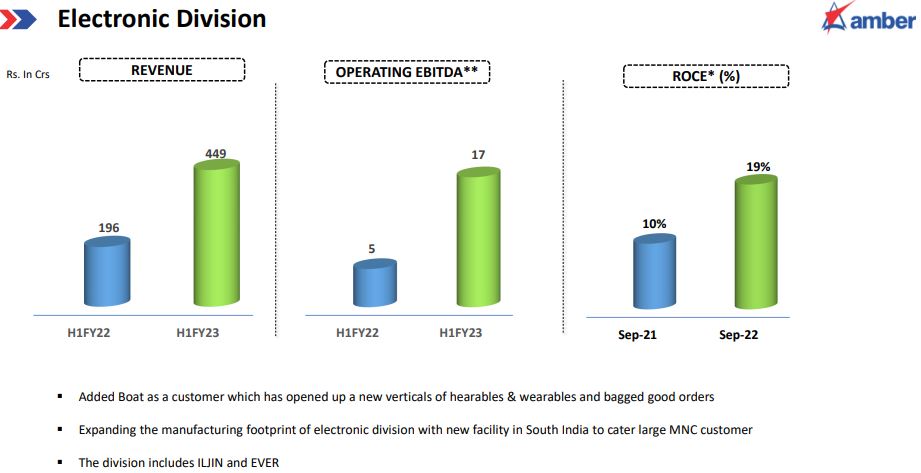

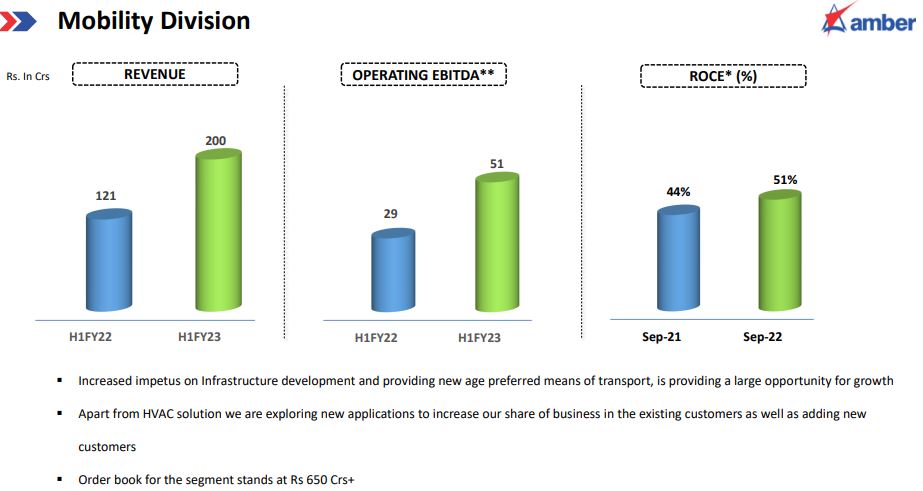

- RAC & Components, Motors, Electronics & Mobility Division contributes 70%, 5%,17% and 8% respectively to the total revenue.

- RAC & Component Division

- Motor Division

- Electronic Division

- Mobility Division

- Other businesses have not seasonality issue as in RAC businesses

- Capex estimated for FY23 is Rs.600 Cr (earlier planned for Rs.400 Cr Only)

- Sluggish demand from July to Sep due to BEE rating change

- Q3 and Q4 will be better than Q2 due to better demand prospective and clients getting ready with heavy inventory for next season in advance

- PLI application is already approved in past quarter. There is no delay in threshold limit of investment and incremental sales. This Year PLI benefit will receive in next year.

- PLI benefit 1st Year Rs.15 Cr and next year Rs.30 Cr

- Higher debt due to capex and seasonality in business (have larger credit period from creditors and get paid during off season). Debt will normalize by year end

- Now, 30% of Total business is non-seasonal and margin accretive

Source: