- Q4 Consolidated Revenue up 55%, Net Profit up 81%

- EBITDA Margins 6.8% Vs 6.9% YoY

- Being a complete solution providers company want investors to focus on this absolute growth of EBITDA by 25%-30% instead of EBITDA Margin

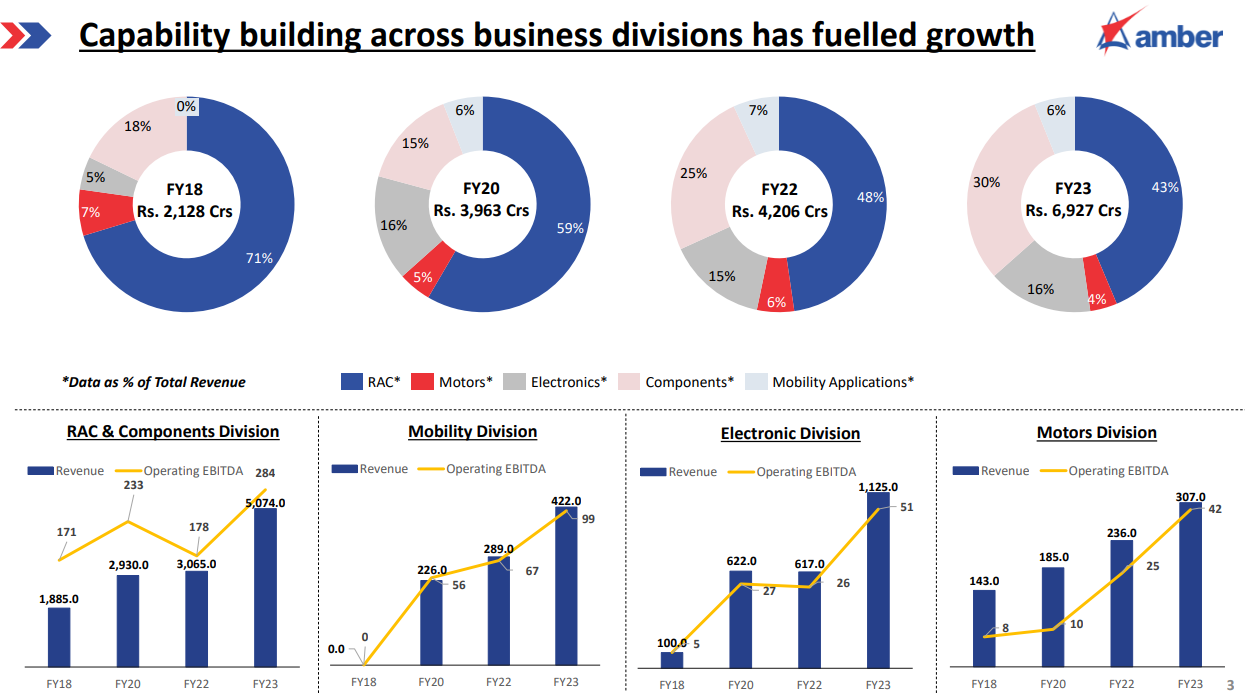

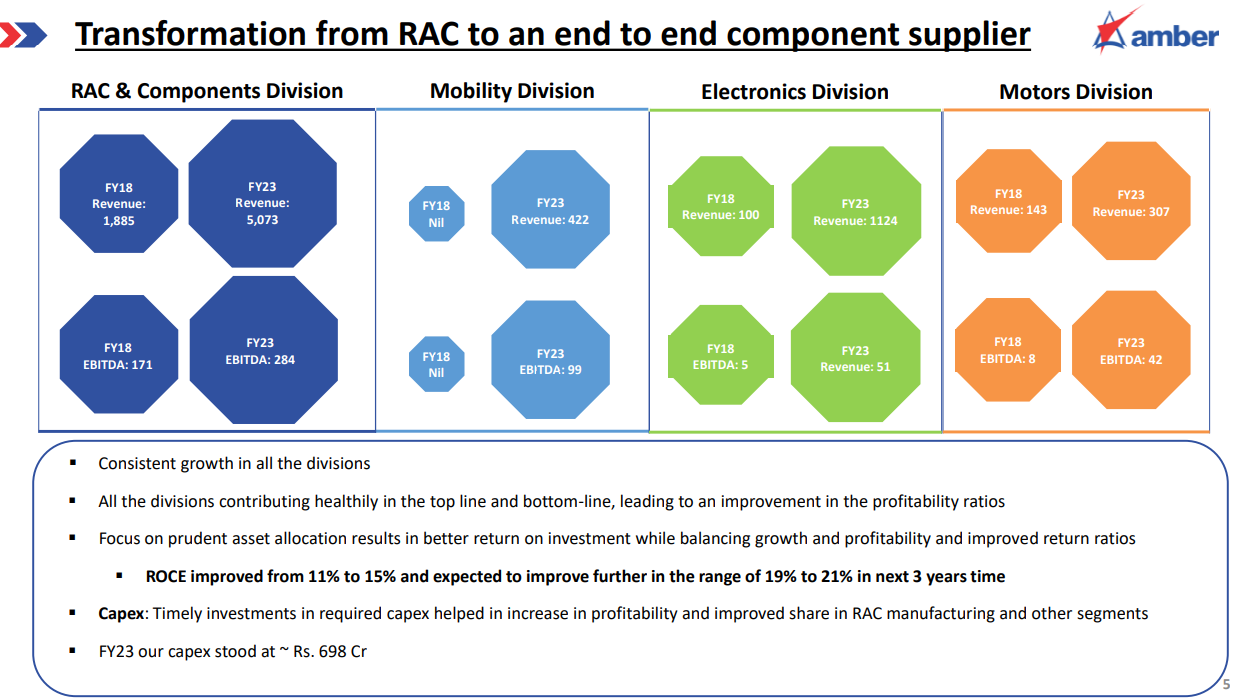

- Year 2018: Total Revenue Rs.2128 Cr, Business Division: RAC 71%, Motor 7%, Electronic 5%, Component 18%, Mobility 0%

- Year 2023: Total Revenue Rs.6927 Cr, Business Division: RAC 43%, Motor 4%, Electronic 16%, Component 30%, Mobility 6%

- ROCE improved from11% to 15%, target of 19 to 21% ROCE in next 2-3 years

- RAC and Component division expected to grow faster than the industry growth rate in FY24

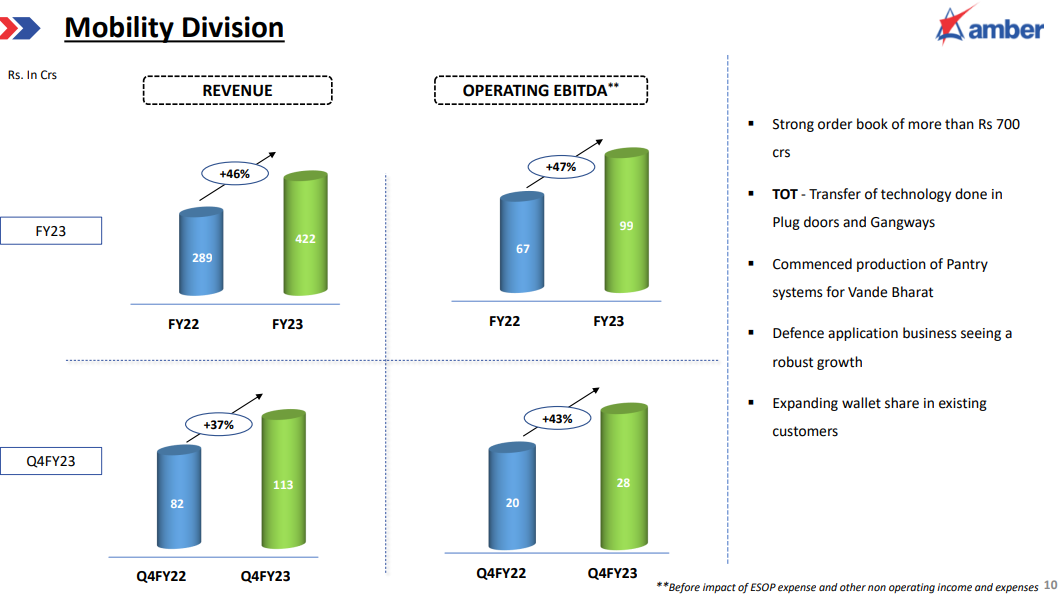

- Mobility Application division is expected to grow at 15%-20%

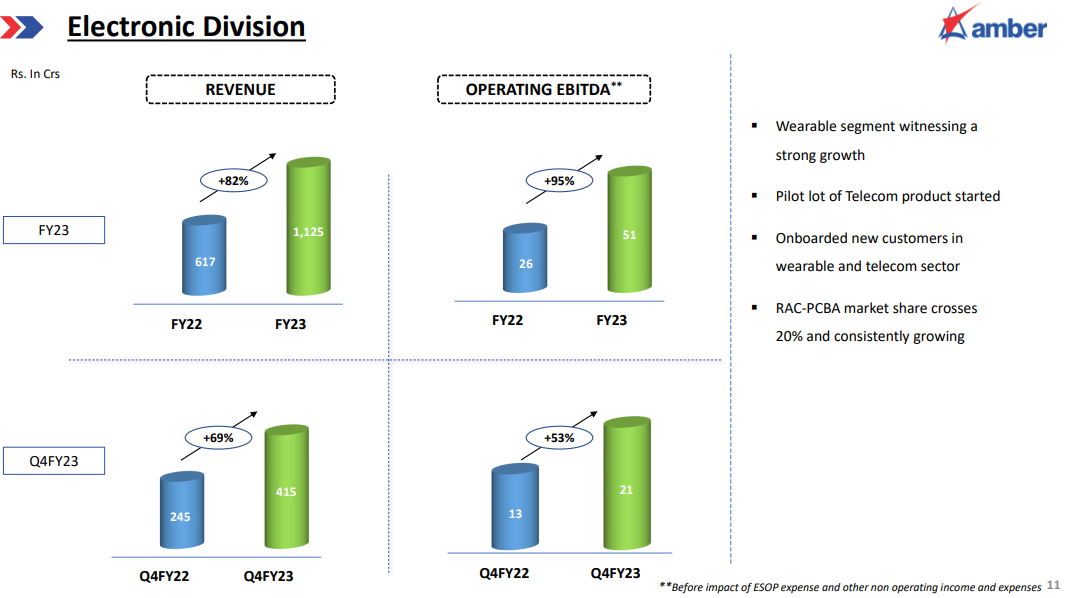

- Electronic division is expected to grow at 35%-40% in FY24

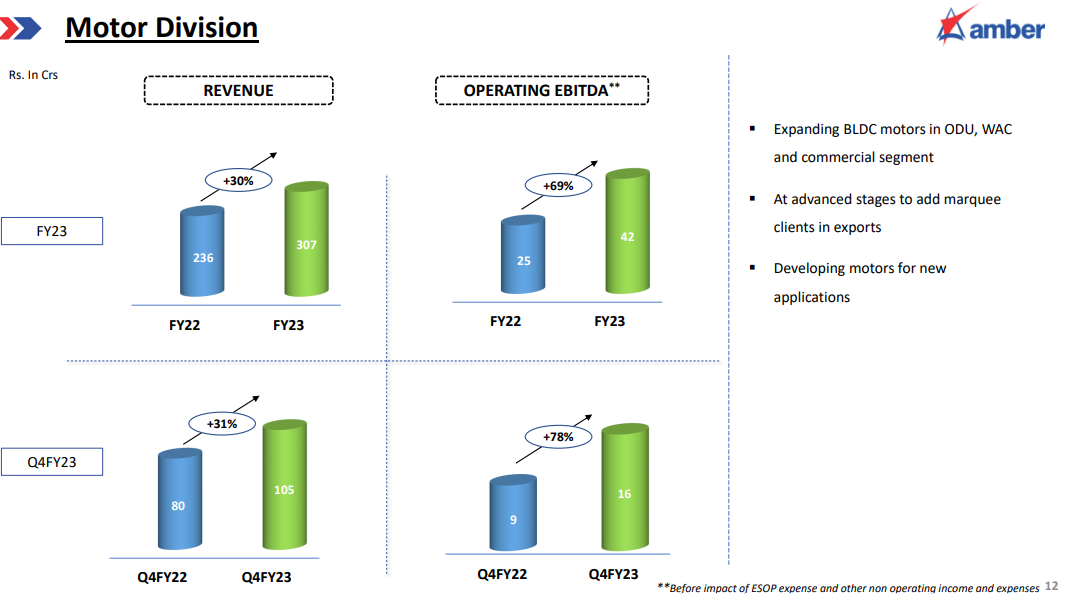

- Motors division is expected to grow at 30%-35% in FY24

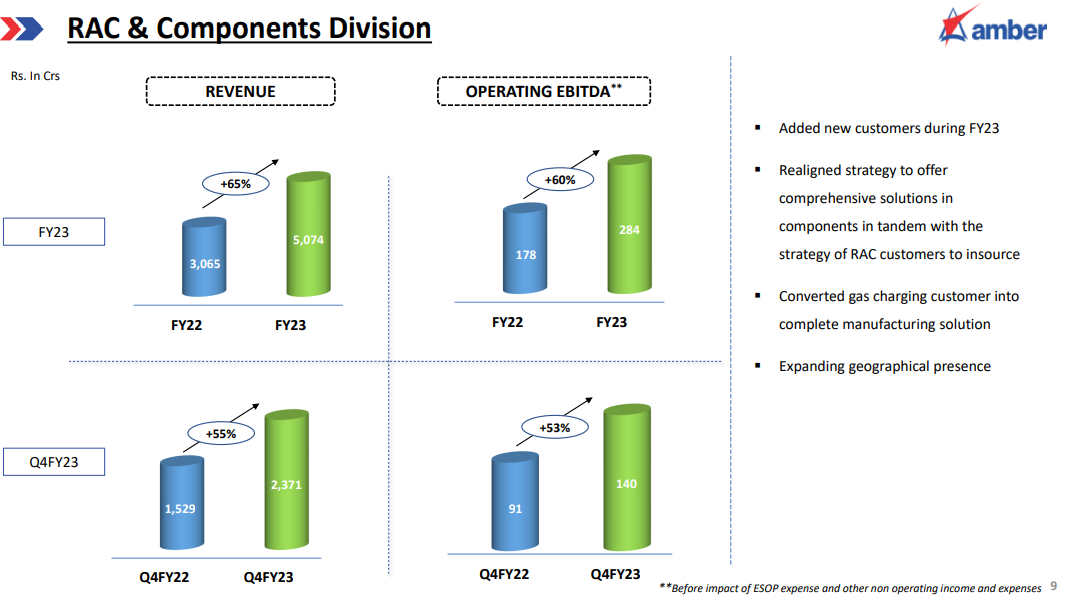

- Transformation from RAC to an end-to-end component supplier

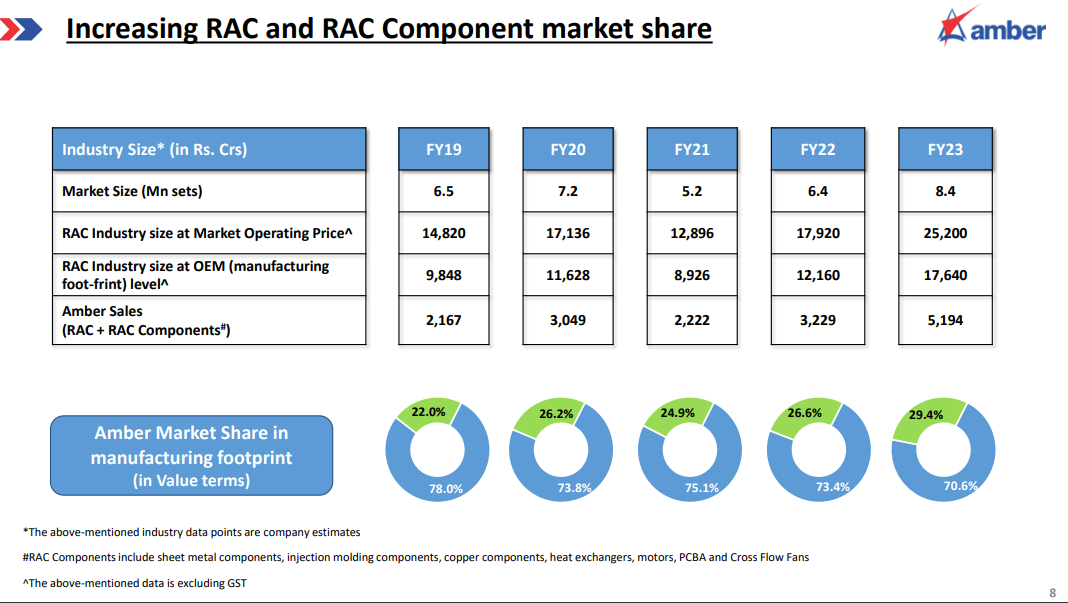

- Amber Market share in RAC+ RAC Components increased from 22% in FY19 to 29.4% (Last year in FY22 it was 26.6%)

- FY23 Capex was Rs.698Cr. For FY24 Rs.350 Cr to Rs.375 Cr (R&D and Maintenance Capex and for expansion in subsidiaries)

- Not planning for any heavy capex as did in last 2 years at least for next 2-3 years

- Net Debt Level at end of FY23 Rs.588Cr(Q3 Concall Comment: Net Debt level is Rs.900 Cr at present where as we expect to close FY23 at Rs.450 Cr to Rs.500 Cr.) Further by end of FY24 Net Debt Level will reduce by Rs.100 Cr to Rs.250Cr

- PLI Update: This financial year we will get first part of Incentives as we have already crossed capex which was required as well as incremental sales

- ESOP Cost for FY23 is Rs.27 Cr and for FY24 it will be around Rs.18 to Rs.19 Cr

- Capacity Utilization on blended basis is around 65% to 70%

- Industry was fearful about Amber’s Customers has started inhouse production but we have supplied component and outpaced industry growth.

Source: