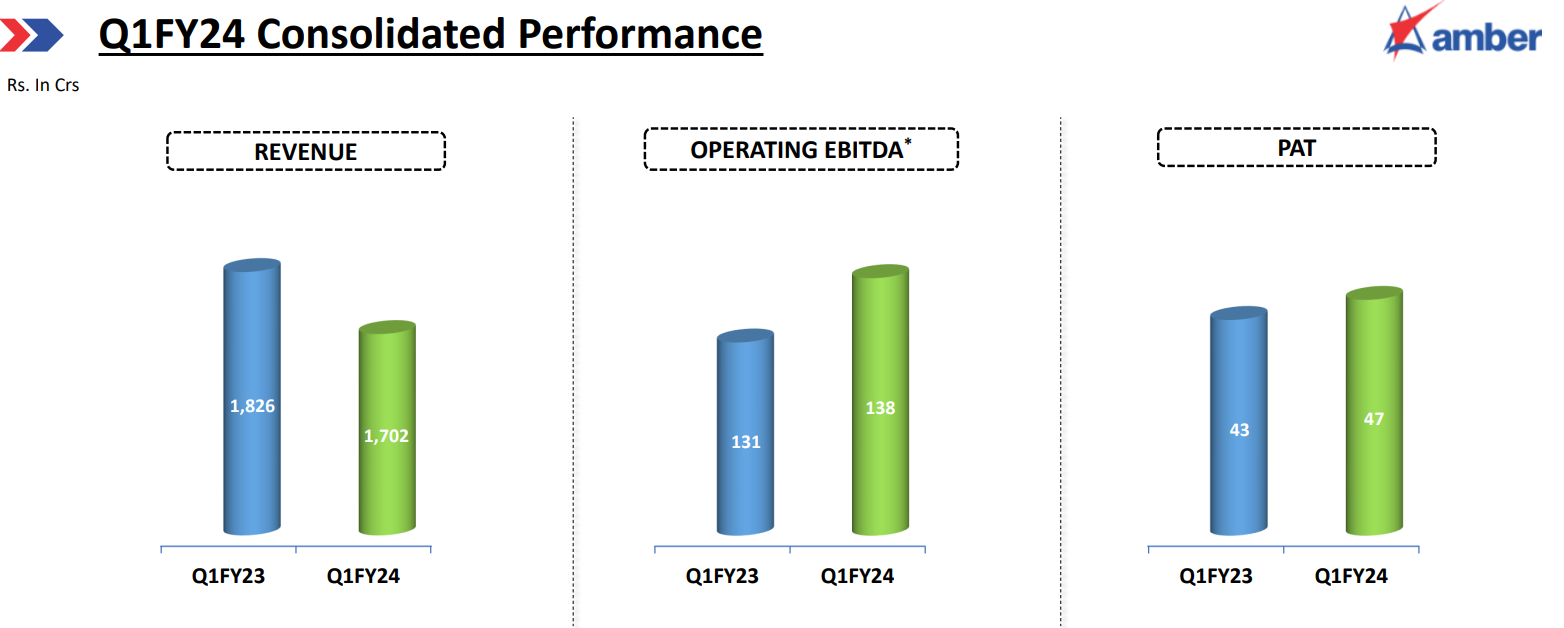

- Q1 Consolidated Revenue down 6%, Net Profit up 8%

- EBITDA Margins 8% Vs 5.4% YoY

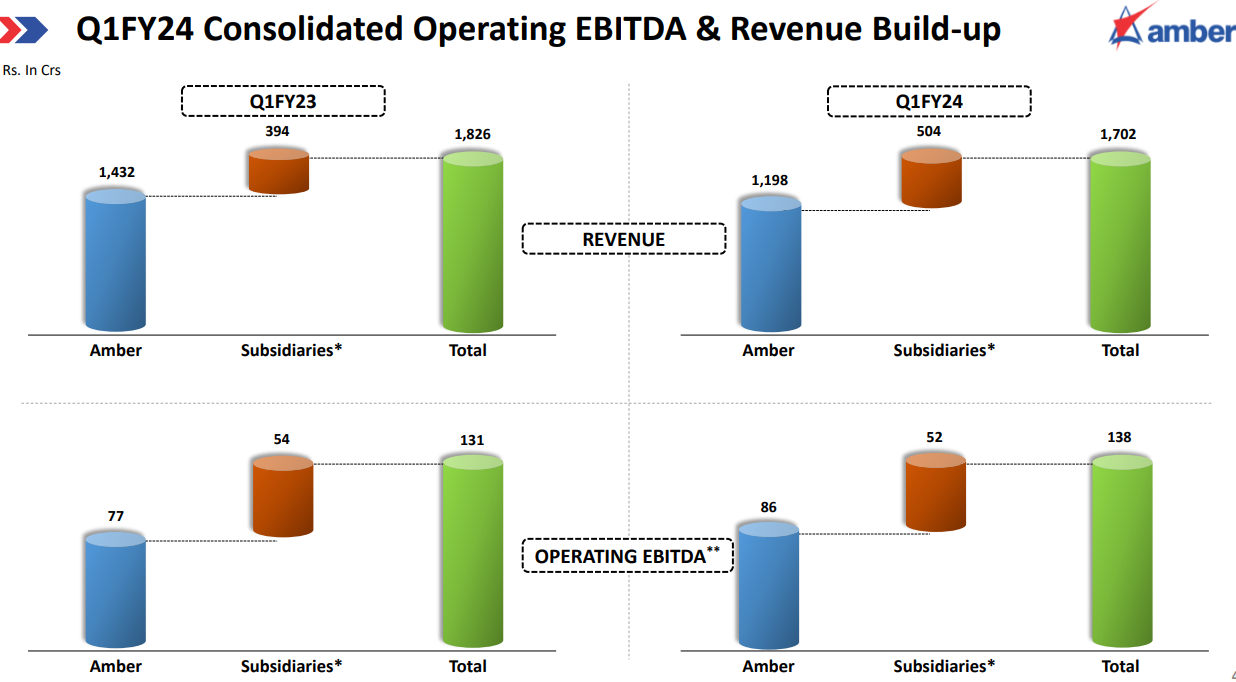

- Component strategy which led to product mix change has helped to improve margins during the quarter despite weak demand in RAC owing to unseasonal weather pattern

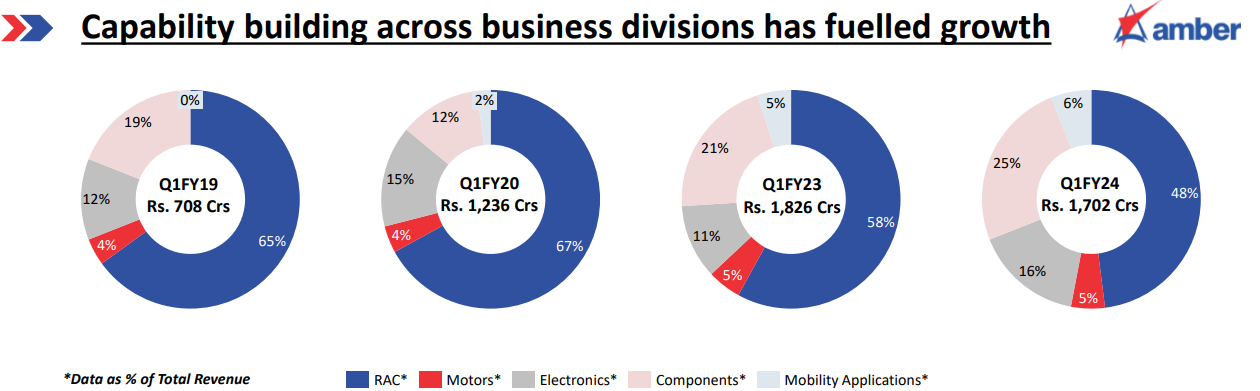

- Q1FY19: Total Revenue Rs.708 Cr, Business Division: RAC 65%, Motor 4%, Electronic 12%, Component 19%, Mobility 0%

- Q1FY24: Total Revenue Rs.1702 Cr, Business Division: RAC 48%, Motor 5%, Electronic 16%, Component 25%, Mobility 6%

- Q1FY24 muted demand due to unseasonal rain has caused elevated channel inventory which will normalize by Q2FY24.

- In H1CY23, RAC Industry has declined by 20% to 25%

- Expect industry to grow by 7% to 8% in FY24

- Strong demand in Mobility with rise of transport infra (Railways & Metros)

- Due to Govt thrust to manufacture electronics locally electronic division is poised for multifold growth opportunity

- RAC and Component division expected to grow faster than the industry growth rate in FY24

- Mobility Division: Sustainable margins are 20% to 22%. Expected to grow 15 to 20% in FY24

- Electronic division is expected to grow at 35%-40% in FY24

- Motors division is expected to grow at 20%-25% in FY24

- Electronic division current margins are 5% and we are targeting for 6% margins in next 2 years

- Net Debt Rs.788 Cr as on 30th Capex done in Rs.40Cr in Q1FY24. Capex for FY24 Rs.350 Cr to Rs.380 Cr Capex.

- ROCE reached to 15% last year itself (Other income included in EBIT). By FY24 end it will be 16% to 17% and By end of next two years will attain ROCE of 19% to 20%

Source: