- Q1 Consolidated Revenue up 157% and Net Profit up 275% YoY

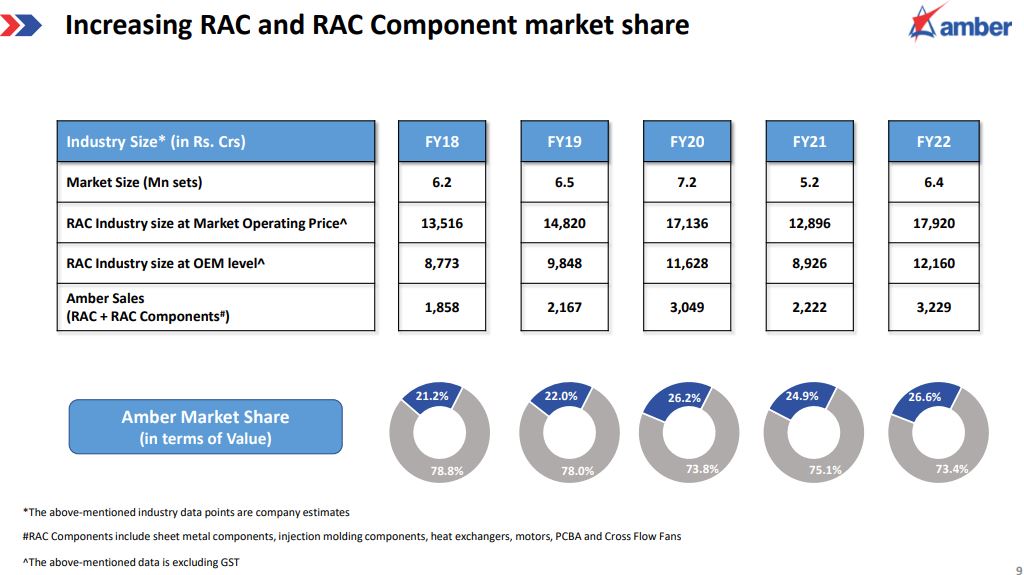

- Having Market share of 26.6%

- From 1st July 2022 revision in BEE rating will increase AC prices

- Will reach the PLI threshold level and qualify PLI Incentives for 1st year

- New SriCity Plant will be operational during H2 FY23

- RAC and Component division expected to grow faster than industry in FY23

- Motor Division is expected to grow more than 30%

- Electronic Division – More than 35%

- Mobility Application Division – More than 15%

- AmberPR and Pravartaka – More than 25%

- ROCE is expected to come back to 17%-20% in next 2-3 years despite capex in growth

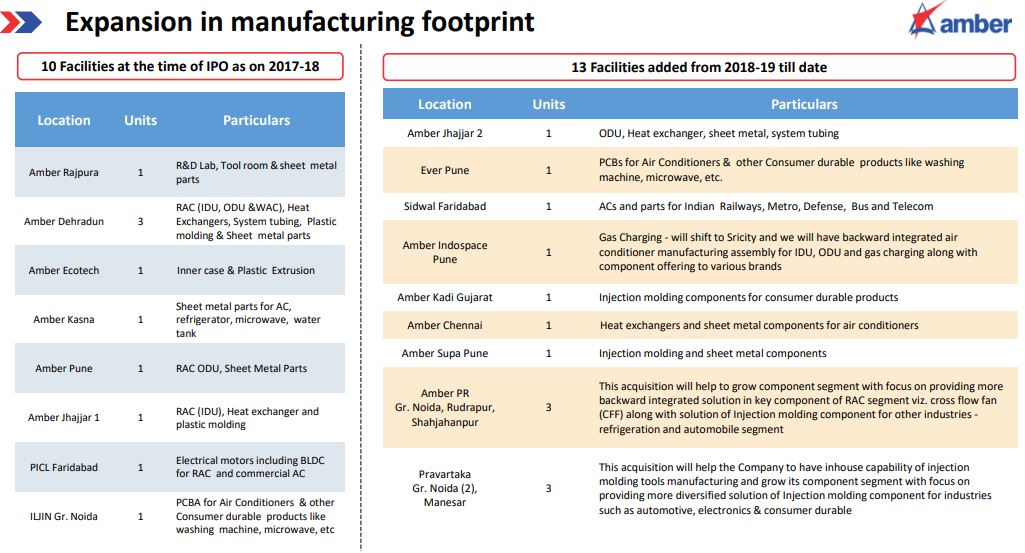

- Before IPO (2018) Amber was having 10 Manufacturing Units. From 2018 till date 13 new facilities added

- In FY22-23 Industry is expecting to surpass 8million RAC Units

- In Q1FY23 RAC Units manufactured by Amber is 1.28M

- Capex for FY23 Rs.400 Cr

- Net Debt Rs.625 Cr, Gross Debt Rs.1300 Cr

Source: